Q3 2025 Market Reports

Industrial

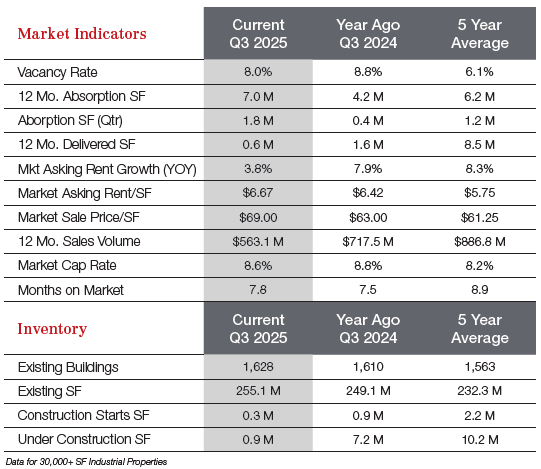

South Carolina’s Upstate remains a premier destination for manufacturers and distributors, particularly those tied to the automotive industry near BMW’s Plant Spartanburg. After a historic supply wave adding over 11 million SF since 2023, the market is stabilizing with steady vacancy rates and rebounding leasing activity. Spartanburg has seen over 10 million SF in 12-month leasing—up 20% from last quarter—driven by a mix of logistics and manufacturing tenants like DHL, Eaton, and ZF Chassis Systems. New construction has slowed considerably, with most space preleased. While large-format buildings still hold higher availability, rates are improving, and smaller spaces remain tight. Affordable rents—nearly 30% below regional peers—continue to attract tenants. As supply eases and demand persists, the Upstate industrial market is positioned for gradual tightening and sustained long-term growth.

READ FULL INDUSTRIAL REPORT HERE

Office

Greenville’s office market continues to benefit from the region’s strong economic and population growth, driven by its manufacturing and logistics base. As Greenville evolves into a key regional hub, office-using sectors such as financial, professional, and administrative services have expanded. The office availability rate remains below the national average at 8.8%, supported by more than 12% job growth over the past five years. A few large leases earlier in the year, including Advanced Technology Systems’ 30,375 SF renewal and CPS Greenville’s 21,000 SF lease, helped stabilize absorption. However, sublease space—such as 138,000 SF listed by Current—has slightly loosened availabilities. Asking rents average $23/SF, with top downtown space reaching the mid-$30s, while suburban rates remain more affordable. Rent growth of 2.9% annually is sustained by limited new supply, as only about 70,000 SF is under construction, mostly preleased.

Retail

Greenville’s retail market remains resilient amid strong population and job growth that continues to outpace national trends. While store closures and bankruptcies created some near-term headwinds, the market’s availability rate remains low at 3.9%, supported by consistent leasing demand of roughly 1.3 million SF annually. Experiential and service-based retailers have quickly filled vacated big-box space, while elevated construction costs have kept new development limited—just 79,000 SF is underway, well below pre-pandemic levels. Annual rent growth of 4.8% continues to outpace national averages, sustaining investor interest despite higher financing costs.